If I ask you that one thing you have always wanted to have no matter how important other needs are, what’s the first thing that would enter your mind? The answer lies in the statistics about the cost of buying a house. According to stats and survey, it has been discovered that “having a house of your own” is the one thing people need the most. Now that’s exactly the thing you have been thinking about, right?

“Having your own house”, no matter how young or old you are and no matter how big or small the house is, is still a dream for everybody.

Now I suppose the purpose of yours to come up to this blog is a little different from thinking to buy a house. Well, congratulations to be finally able to get the house of your dreams and for those who are thinking about buying a house, this place is perfect for you all because here we are going to clear your every doubt about the “cost of buying a house” of your dreams. From building a dream in your head to finally paying for the house, everything is written for you here to help put a smile on your face, let your inner confidence grow and finally be able to say,” I bought my own house”.

Is it making your heart skip a beat and nervous at the same time?

So, without taking the further time of yours, let us take you to the very step involved in the cost of buying a house; –

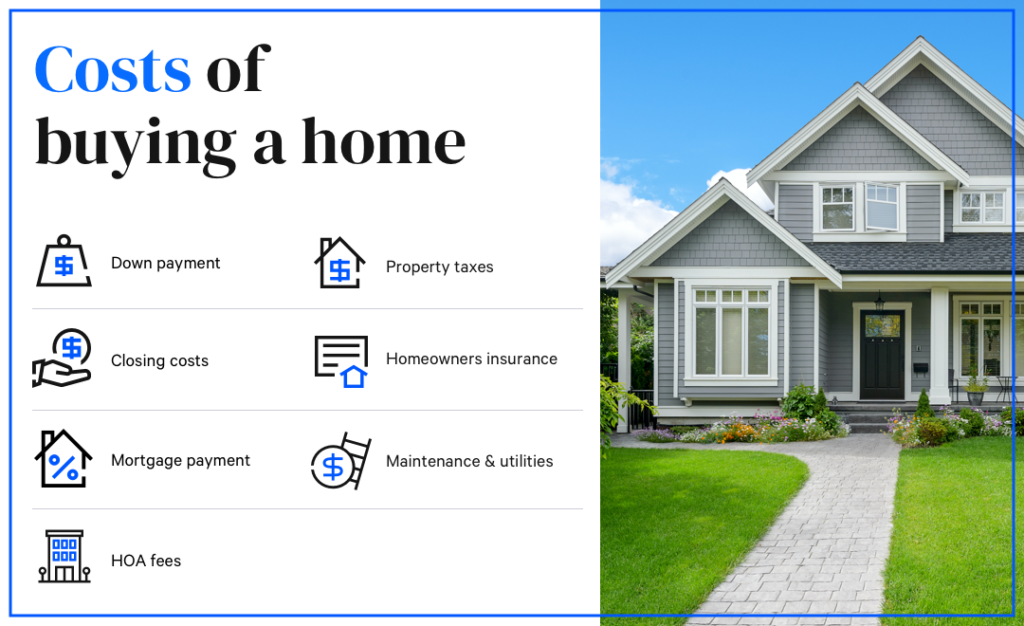

Arranging down payment-

Down payment is the payment made in the initial years of buying something and the rest of the payment is made later. While buying a house, we are required to pay 15-20% of the down payment for the house right at the moment we decide to buy a house or a plot. Now to save this much amount for starting your dream, you must initially start saving and investing according to your best fit. Usually, you can raise money from a bank as a bank loan in name of some security but it is advisable to have some savings to kickstart your dream of buying a house with ease. Because delaying in arranging down payment means delaying on your dream to buy a house.

Now there are a few pros and cons about the amount of down payment you can accumulate. For instance, say if the amount you can raise is huge in amount, your dependency on the borrowed funds i.e. loans would be reduced thus giving you an advantage for saving some money for the home loan insurance as well. But if you can arrange only a handful of amounts, then you’ll have to depend more on the external credit.

MODT Charges –

“Memorandum for Deposit of Title Deed” is an undertaking given by you stating that you have deposited all the documents to the lender. It is a kind of home loan charge and the government also imposes stamp duty on this. The benefit of charging a MODT is that the rate of commission imposed over this is way less i.e. 0.1% which makes it easier for anyone to go with.

Stamp duty and charges

– having a stamp duty and paying registration charges for your house is like the legal evidence of your ownership for the house. Registration and possession of a house is a very important element in setting up your house. You can get your property registered in the local municipal records. As a tax, you will be asked to some amount as “stamp duty charges”.

Now, what exactly is “stamp duty”? Stamp duty is a tax levied by the government on physical property. It is a completely proper and legal document and is also admitted as evidence in the courts. Thus, whether it is an under-constructed house or rented house, you are supposed to pay the stamp and registration value for the physical and evident possession of your house.

Brokerage charges

– If you have taken a broker’s help in finding the house and its construction, he will charge you some per cent of your money as his reward i.e. brokerage charge. It is the commission he earns in the entire process of settling your house. This fee varies from broker to broker and from place to place. If the broker is the same person involved in the buying and selling aspect, he may charge a little less or vice versa.

Home-loan charges

– apart from the amount of money spent on building a house, there are other costs involved in the entire process. One of them is “Home Loan Charges”. These charges include “interest charges” from the bank, loan processing fees, late payment charges, application fees or legal fees. These all are the legal charges you are ought to pay either to the bank or the desired organisation.

Parking charges

– while you buy a house, you also desire to have your parking place whether inside or outside the boundaries of your house. You can get your spot by paying a handsome amount of money. (valium) The charge over this depends upon the type of property you are acquiring. For instance, a more luxurious house demands a greater value for the parking spot and vice versa.

Interior and other management charges

– Now once you enter your newly build house, it is not the end to the amount you spent. There is still a lot of things needed to be taken care of. For example – the furnishing and the ventilation of the house, the furniture, the setup of the house and so on. The costs involved in all these are also a matter of fact on your spending limit. Also, all the overhead expenses are to be borne by the home-owner. Now, this completely depends on you, how you would like to decorate your house and what elements you want and can adjust your budget according to that.

By now, I hope that all of your doubts related to the cost of buying a house are clear and your mind is free from a whole lot of information.

All the data presented above can be used trusted and used to your best potential.

Have happy planning for your house!